How Retirement Solutions, Inc. Allocates Your Savings with NextPhase™

A clear investing approach for creating lasting, inflation-adjusted retirement income

Ask Yourself These Questions:

How much can I safely spend?

How much investment risk can I handle?

Are my retirement savings in the right place?

Do I have enough retirement savings to last my lifetime?

Meet NextPhase™

The Strategy

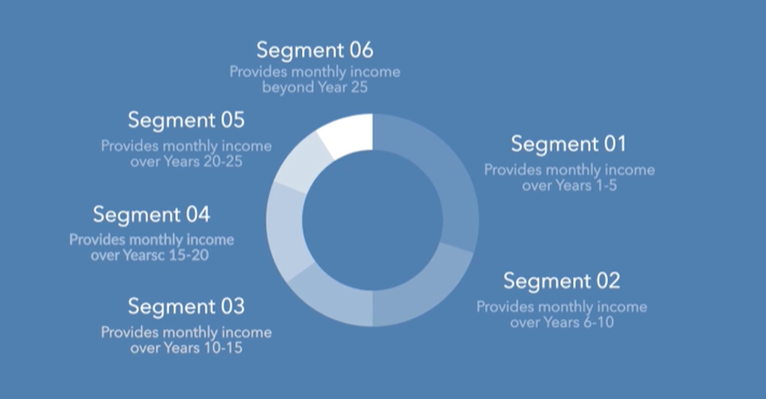

Your financial advisor will set up a series of income-producing segments, seeking to provide specific amounts of income over the course of your retirement. Optional components for emergencies, or longevity planning, can be incorporated.

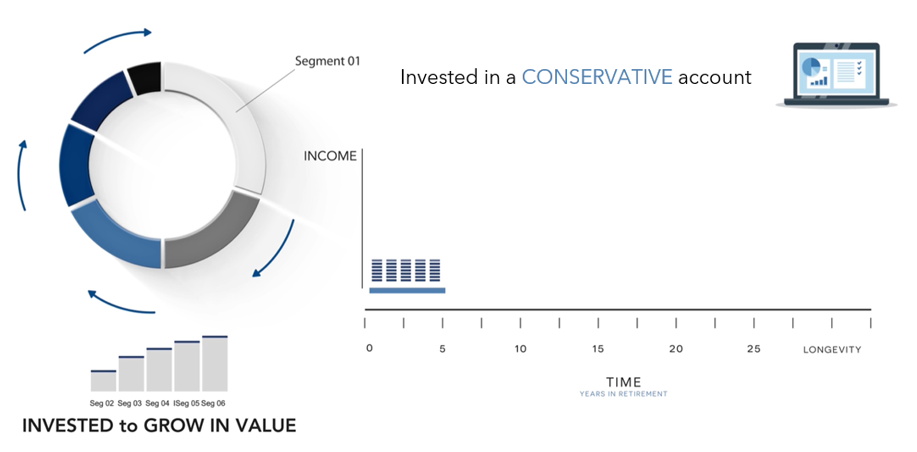

Segment 1

Segment 1 is invested in a conservative account, used to provide monthly income over the first five years of the plan. Generating predictable income from a conservative account is an ideal way to get off to a good start in retirement. While Segment 1 provides income, the other segments are invested to grow in value, until it is their turn to be converted into a conservative account, and provide predictable monthly income.

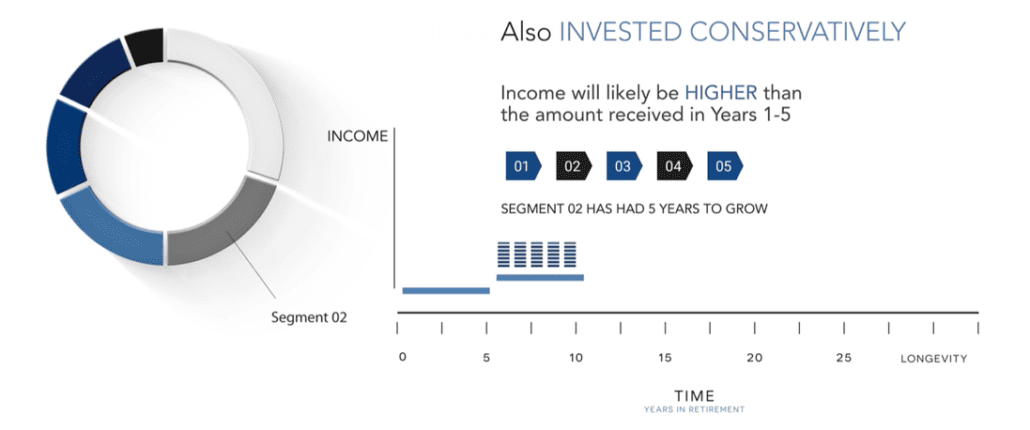

Segment 2

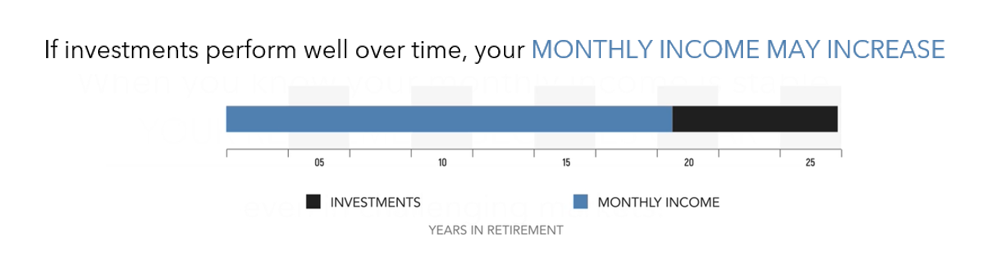

Segment 2, also invested conservatively, will provide income in years 6-10 of retirement. The income in those years will likely be higher than the amount received in Years 1-5. That’s because segment 2 had 5 years to grow, and when converted, it will provide inflation-adjusted income.

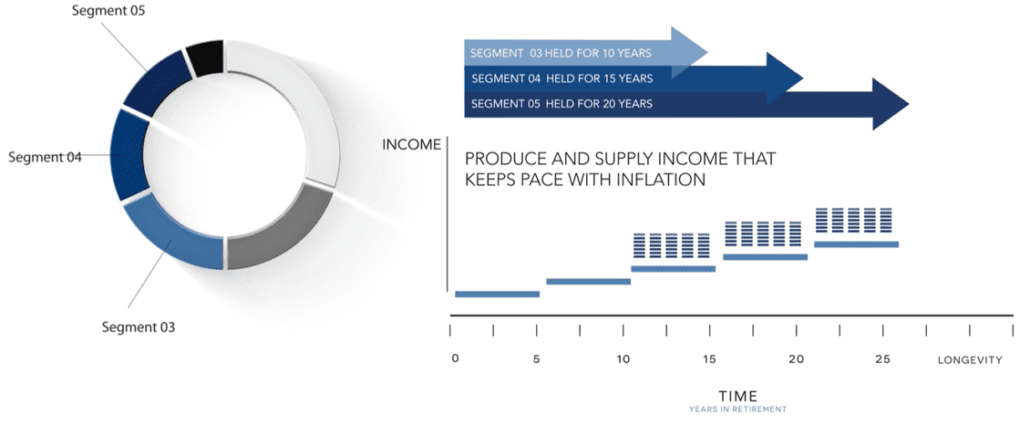

Segments 3, 4, 5

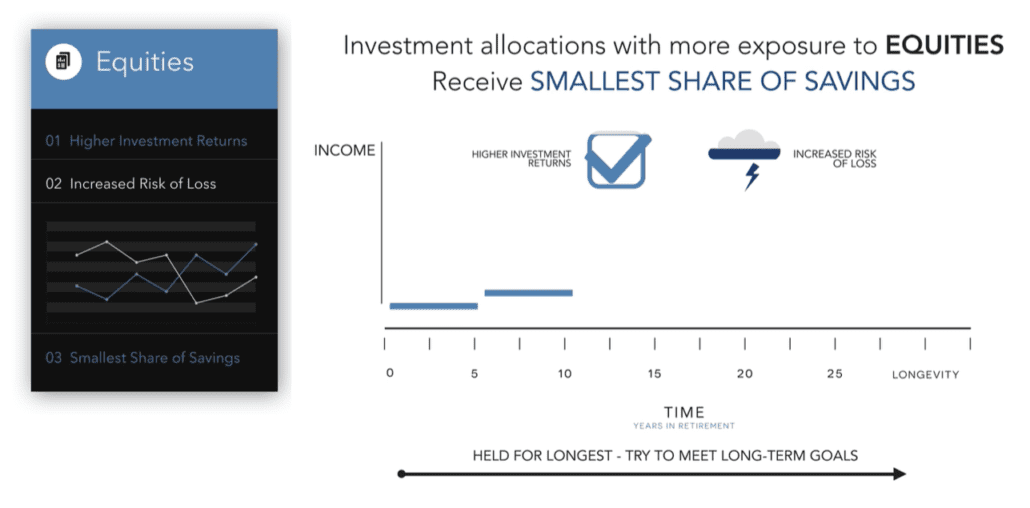

Segments 3, 4 and 5 contain investment allocations with more exposure to equities. Retirees investing in equities seek to achieve higher investment returns with increased risk of loss. Holding these accounts for the longest periods of time increases the chances of meeting long-term goals. The smallest share of your savings will usually be put in segments that seek the highest returns, and are held for the longest period.Segment 3 is held for 10 years, Segment 4 for 15 years, and Segment 5 for 20 years. Together, these three segments are earmarked to produce income that, if their investment return objectives are met, will keep pace with inflation. When it becomes time to access a segment to draw income from, the money will be placed in a conservative investment account, just like Segment 1, to help continue your predictable monthly income.

When you know your monthly income is predictable, your retirement becomes clear, even in challenging markets!

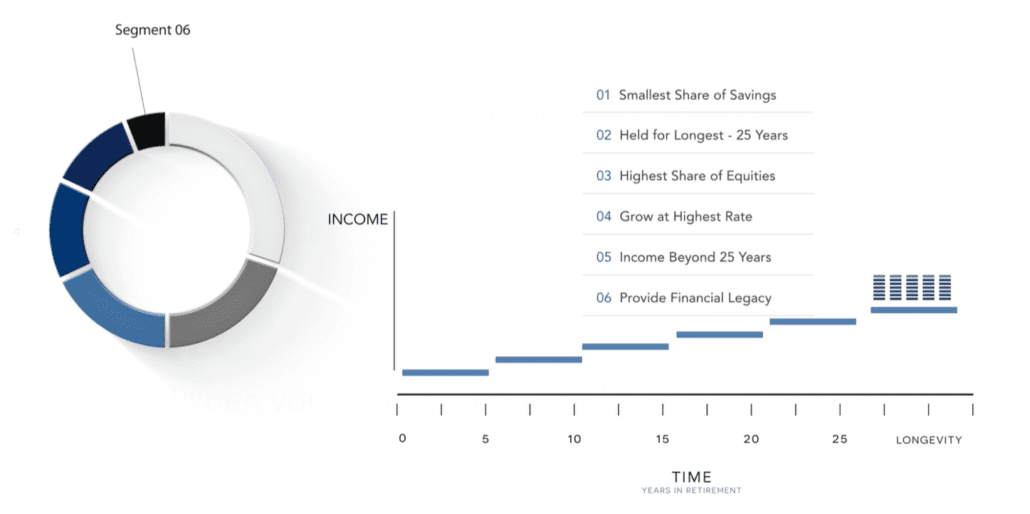

Segment 6

The final segment is the pool that often receives the smallest share of savings, but is held for the longest time – typically 25 years. The objective is to grow at the highest rate, and is available to provide additional income, beyond 25 years. Or provide the financial legacy you desire to leave to children, grandkids, or your favorite charity.

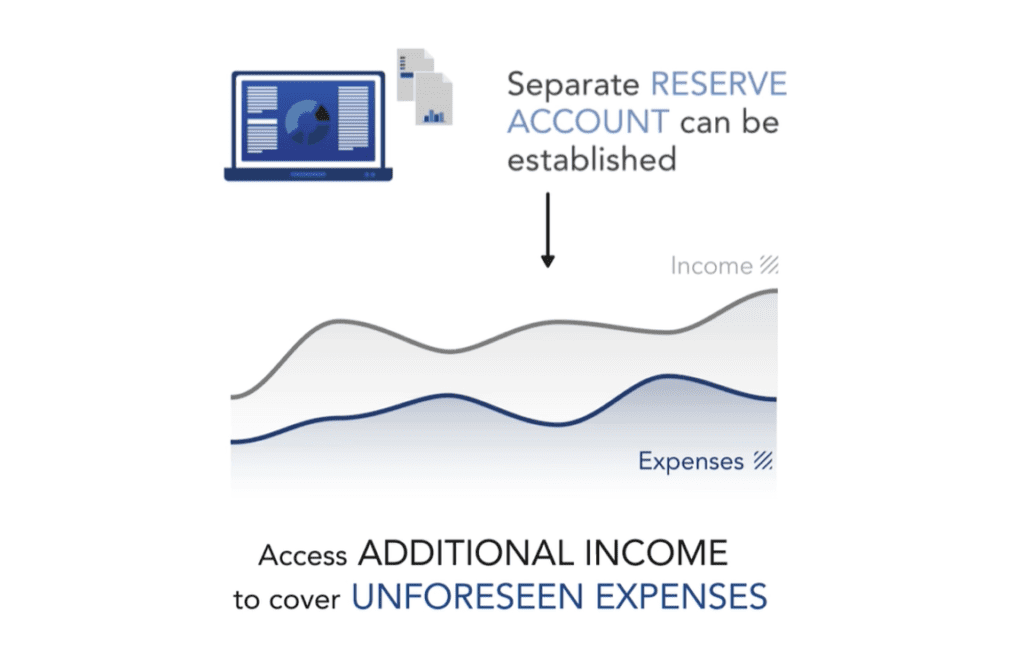

What If I Have An Emergency Need?

A separate reserve account can be established to access additional income to cover unforeseen expenses not budgeted for at the beginning of your plan. Your financial advisor will discuss the need for this account, and the amount you might want to set aside for unplanned expenses.

Will I Have Enough Money to Last My Lifetime?

Longevity can create a serious financial risk, because whatever the age, no retiree stops needing income. You probably know someone in their late 80s or 90s. To manage the risk of running out of money, another optional component is to add a Longevity Strategy. Longevity planning starts by allocating a portion of your retirement savings to an annuity to provide a lifetime stream of income.

If the equities in longer-term segments don’t perform well, the monthly income from your longevity strategy acts as a backup to help you meet your monthly expenses. This is an example of transferring a measure of risk away from you, and to an insurance company.

Want to see it work for you?

Don’t enter retirement without a clear plan for generating what no retiree can go without – income that lasts!

Investing involves risk, and you may incur a profit or a loss. There is no guarantee that NextPhase will perform as planned. If the strategy underperforms, the income levels and assets could be significantly reduced.

When utilizing annuities for guaranteed income, these guarantees are based on the claims paying ability of the issuing company.

Timing Risk is a trademark of Wealth2k, Inc. What’s My Income? is a registered trademark of Wealth2k, Inc.

https://2rsi.com/wp-content/uploads/2022/12/pexels-fauxels-3184292-scaled.jpg14402560Retirement Solutions Inc. Teamhttps://2rsi.com/wp-content/uploads/2022/07/RSI_Brand-Identity_RGB_Signature_Full-Color-1030x423.pngRetirement Solutions Inc. Team2022-12-30 14:59:112024-10-04 10:05:56How Retirement Solutions, Inc. Allocates Your Savings with NextPhase™

We may request cookies to be set on your device. We use cookies to let us know when you visit our websites, how you interact with us, to enrich your user experience, and to customize your relationship with our website.

Click on the different category headings to find out more. You can also change some of your preferences. Note that blocking some types of cookies may impact your experience on our websites and the services we are able to offer.

Essential Website Cookies

These cookies are strictly necessary to provide you with services available through our website and to use some of its features.

Because these cookies are strictly necessary to deliver the website, refusing them will have impact how our site functions. You always can block or delete cookies by changing your browser settings and force blocking all cookies on this website. But this will always prompt you to accept/refuse cookies when revisiting our site.

We fully respect if you want to refuse cookies but to avoid asking you again and again kindly allow us to store a cookie for that. You are free to opt out any time or opt in for other cookies to get a better experience. If you refuse cookies we will remove all set cookies in our domain.

We provide you with a list of stored cookies on your computer in our domain so you can check what we stored. Due to security reasons we are not able to show or modify cookies from other domains. You can check these in your browser security settings.

Google Analytics Cookies

These cookies collect information that is used either in aggregate form to help us understand how our website is being used or how effective our marketing campaigns are, or to help us customize our website and application for you in order to enhance your experience.

If you do not want that we track your visit to our site you can disable tracking in your browser here:

Other external services

We also use different external services like Google Webfonts, Google Maps, and external Video providers. Since these providers may collect personal data like your IP address we allow you to block them here. Please be aware that this might heavily reduce the functionality and appearance of our site. Changes will take effect once you reload the page.

Google Webfont Settings:

Google Map Settings:

Google reCaptcha Settings:

Vimeo and Youtube video embeds:

Other cookies

The following cookies are also needed - You can choose if you want to allow them:

Privacy Policy

You can read about our cookies and privacy settings in detail on our Privacy Policy Page.